You Can't Afford to Wait - Uni student's guide to start investing.

- Vansh Mittal

- May 10

- 7 min read

Analyst : Vansh Mittal

Editor : Vansh Mittal

Published : 10th May 2026

The Lion Brief

Investing 101 : A Beginner's Guide for Australian Uni Students

"The best time to start investing was ten years ago. The second best time is today — but only if you understand what you're doing."

What is Investing?

Investing is the act of putting your money to work so that it grows over time, rather than sitting idle in a bank account losing purchasing power. That last part is critical. In 2026, with inflation running above 4% annually and the average savings account paying 2–3%, parking your money in cash is not a neutral act. It is a slow, guaranteed loss of real value.

For a university student, this often feels abstract. You might be working casual shifts, studying full-time, and struggling to keep rent paid and groceries stocked. Investing feels like something for people with salaries, not for someone in their second year of commerce at a share house in Brunswick or Ultimo.

But here is the structural truth that most financial education fails to communicate early enough: the decisions you make — or don't make — between the ages of 18 and 25 will have a larger compounding financial impact than almost any decision you make later in life. That is not motivational rhetoric. It is a mathematical consequence of time, and it has a name: compound interest.

"Wages that aren't keeping pace with living costs limits people's ability to save, making the transition from renting to home ownership increasingly hard." — Arielle Executive, 2026

Key Statistics

The Main Asset Classes : Where You Invest

An asset class is a category of investment with distinct characteristics — different return profiles, risk levels, liquidity, and market behaviours. Understanding the major asset classes is the foundation of building any portfolio. Each suits different timeframes, temperaments, and financial situations.

Come under two categories : Traditional Investments and Alternative Investments.

NOTE : For all of these asset classes / types, a separate informative report will be made available soon. Exploring all of these asset classes in depth.

Traditional Investments :

Shares (Equities) - Fractional ownership stake in a publicly traded company. Return comes from capital-growth as well as dividends.

ETFs (Exchange-Traded Funds) - A basket of shares collected into a single security trading on the exchange just like a normal share.

Bonds - A debt instrument. Lending money to a government or a big corporation in exchange for fixed interest payments monthly or annually and principal at maturity.

Alternative Investments :

Real Estate - Australia's most culturally entrenched asset class. Even not directly purchasing property, exposure can be gained through A-REIT (Australian Real Estate Investment Trust) which are listed funds like ETFs.

Private Credit - Loans made directly to businesses or startups outside the traditional banking system - typically small to medium enterprises with less exposure to public funds.

Cryptocurrency - The largest dominance in Gen Z financial conversations. Includes assets like Bitcoin, Ethereum, and thousand others. New coins are generated every second. Even you can build one on your own.

Commodities - Includes hard physical goods like gold, silver, oil; and soft goods like soybean, wheat, cocoa etc. These are accessed by holding ETFs instead of holding the actual physical goods.

Hedge Funds - Hedge funds are private, pooled investment vehicles that use complex, active strategies—such as leverage, derivatives, and short selling—to achieve high, positive returns (absolute returns) regardless of market conditions.

Infrastructure - Investing in assets like toll roads, airports, sea ports, utilities, telecom networks etc. These funds traded on the ASX stock exchange and can be accessible using minimum funds.

Collectibles - Art, wine, rare watches, trading cards, vintage sneakers. An asset class many young people already invest in without even realising. Owning things you love also hold value.

Asset Class | What It Is | Historical Return | Risk Level | Min. Entry |

Traditional Asset Classes | ||||

Shares (ASX) | Ownership in listed companies | 7–10% p.a.* | Medium–High | ~$500 |

ETFs | Basket of shares, traded on ASX | 7–9% p.a.* | Medium | ~$100 |

Bonds | Loan to govt/corporation | 3–5% p.a. | Low–Medium | ~$1,000 |

Property (direct) | Physical real estate | 6–8% p.a.* | Medium–High | $500k+ |

A-REITs | Listed property trusts | 6–8% p.a.* | Medium | ~$100 |

Cash/Term Dep. | Bank savings product | 3–5% p.a. | Very Low | Any |

Alternative Asset Classes | ||||

Private Credit | Loans to businesses outside banking system | 8–12% p.a.* | Medium–High | ~$2,000 |

Cryptocurrency | Decentralised digital assets (e.g. Bitcoin) | Highly variable | Very High | ~$10 |

Commodities | Physical goods — gold, oil, agricultural products | 2–5% p.a.* | Medium–High | ~$100 (ETF) |

Hedge Funds | Actively managed, complex strategies | Varies widely | High | $500k+ (typically) |

Infrastructure | Airports, toll roads, utilities (via listed funds) | 6–9% p.a.* | Medium | ~$100 |

Collectibles | Art, wine, watches, cards, rare items | Highly variable | High | Varies |

How To Get Started : The Actual Steps

The infrastructure of investing has become substantially more accessible over the past decade. You no longer need a financial adviser, a minimum balance of $50,000, or a detailed understanding of portfolio theory. The steps below represent the minimum viable path to beginning as an Australian investor.

BEFORE ANYTHING : EDUCATE YOURSELF ABOUT MARKETS, ASSETS, RETURN, RISK, AND ALL THE OTHER BASICS AND PRACTICE ON A DEMO ACCOUNT BEFORE USING REAL MONEY.

Securing A Tax File Number (TFN) : A Tax File Number (TFN) is required for investing in Australia. Without it, investment platforms and your superannuation fund will withhold tax at the highest marginal rate (47%), regardless of your actual tax bracket. Apply through the ATO website at ato.gov.au — the process is free and takes less than fifteen minutes.

Building A Small Emergency Fund First : Before investing a dollar, establishing a cash buffer of at least one to two months of essential expenses in a separate, high-interest savings account is generally helpful. This is not invested — it is held as insurance. The purpose is to prevent you from being forced to sell investments at the worst possible time (when markets are down) because of a sudden expense.

Choosing A Brokerage Platform : A brokerage account is required to buy shares or ETFs. Several platforms now cater specifically to beginners and small investors. The comparison below covers the main options for Australian retail investors.

Platform | Best For | Trade Fee | Min. Investment |

CommSec Pocket | True beginners | $2 under $1k | $50 |

Pearler | Long-term ETF investors | $6.50 flat | $1 |

Stake | ASX + US access | Free (US) / $3 (ASX) | $0.01 |

SelfWealth | Active investors | $9.50 flat | $500 |

Start With Simplicity : The single most common mistake new investors make is building unnecessary complexity. You do not need ten ETFs, sector tilts, and an alternative assets allocation in your first month of investing. A two-fund portfolio — one Australian shares ETF and one global shares ETF — provides meaningful diversification across thousands of companies and a reasonable historical return profile, for a combined fee typically under 0.20% per year.

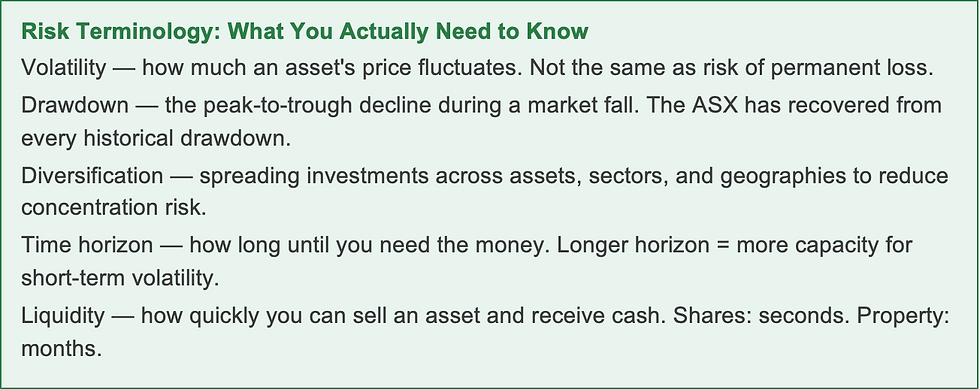

Understanding Risk : The Trade-Off That Shapes Everything

Every investment involves a trade-off between potential return and the risk of loss. This is not a matter of opinion or market philosophy — it is a structural feature of how capital markets function. Higher potential returns always come with higher volatility and higher probability of loss in any given period.

For a young investor with a 40-year time horizon, volatility is not the enemy — panic is. A portfolio that falls 30% in a recession is not destroyed. It is on sale. The investors who were harmed were those who sold at the bottom, locking in losses permanently. The investors who held — or who increased their contributions during downturns — captured the full recovery.

The Silent Tax : The Brokerage Fees Matter more than you think

Investment fees are the most under appreciated variable in long-term wealth building. Because they are expressed as percentages rather than dollar amounts, their magnitude is not intuitively obvious. The table below makes it concrete.

A 1.50% annual fee — typical of actively managed retail funds — costs $42,234 in forgone returns relative to a 0.10% ETF on the same $10,000 over 30 years. The fee is not charged on your original investment. It compounds in reverse, eating into the exponential growth that makes investing valuable in the first place. This is not an argument against all fees — it is an argument for understanding exactly what you are paying and why.

Assumes 8% gross annual return. Fee deducted annually before compounding.

The Common Traps in Investing

Financial education literature focuses heavily on what to do. Equally important — perhaps more important for beginners — is what to avoid. The following traps have derailed more new investors than any market crash.

Trap | Why It's Dangerous |

Investing rent money | Markets can fall 40% and stay down for years. If you need the cash, you'll be forced to sell at the worst time. |

Social media tips | You see gains, never losses. Tips about meme stocks, crypto 'opportunities' and 'next big things' have ended more accounts than built them. |

Market timing | Buying and selling based on short-term predictions. Professional fund managers consistently fail at this — a beginner has near-zero chance. |

Ignoring fees | A 1% fee sounds harmless. On $50,000 over 30 years at 8%, it costs $73,000+ in forgone growth. |

Panic selling | Selling when markets fall locks in losses permanently. The recovery goes to whoever stayed in. |

Over-concentrating | Putting everything into one company, sector, or asset class. Diversification exists precisely to protect against unknown unknowns. |

The Most Important Thing

The single biggest barrier to investing for young Australians is not capital. It is starting. Every week of delay represents compounding time that cannot be recovered. You do not need to understand options pricing, balance sheet analysis, or macroeconomic theory to begin. You need a TFN, a brokerage account, and the discipline to invest regularly into a diversified, low-cost fund.

The people who retire with financial security are not, on average, the ones who made the cleverest trades in their thirties. They are the ones who built boring, consistent investment habits in their twenties — and did not abandon them when markets fell, when something on social media looked more exciting, or when the next big thing offered a shortcut.

"Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it."

Disclaimer: This report is produced for educational and informational purposes only. Nothing contained herein constitutes financial, legal, or investment advice. All statistics and illustrative figures are sourced from publicly available research or are modelled estimates — actual outcomes will vary. Readers should seek advice from a licensed financial adviser before making any financial decisions. The Lion Brief is not a licensed financial adviser.

© 2026 The Lion Brief. All rights reserved.

Comments